By – Shubhendra SIngh Rajawat

New Delhi, February 7, 2025 – The Reserve Bank of India (RBI) has announced a reduction in the repo rate after five years. In the Monetary Policy Committee (MPC) meeting held on February 7, 2025, the new RBI Governor, Sanjay Malhotra, declared a 25 basis points (bps) cut, bringing the repo rate down from 6.5% to 6.25%.

This decision was largely in line with market expectations and is aimed at easing borrowing costs for individuals and businesses. With this reduction, home loan and car loan EMIs are expected to decrease, providing relief to borrowers across the country.

RBI’s Repo Rate Cut: First Reduction in Five Years

The Monetary Policy Committee, after its three-day deliberation, decided to lower the key policy rate by 25 basis points. The last time the RBI reduced the repo rate was during the COVID-19 pandemic in 2020 to stimulate economic activity. Since February 2023, the repo rate had been maintained at 6.5%, marking a period of stability in interest rates.

With the latest cut, the central bank aims to boost economic growth by making loans more affordable, thereby reducing the financial burden on consumers and businesses alike.

How Will the Rate Cut Affect Your Loan EMIs?

A decrease in the repo rate often leads to a reduction in interest rates on home, car, and personal loans. However, the extent of the reduction depends on individual banks, as they adjust their lending rates based on their financial conditions.

Tax expert and senior Chartered Accountant Sanjeev Maheshwari stated, “After a long time, the RBI has cut interest rates, which is expected to provide relief to home loan and personal loan borrowers. However, how much of this cut is passed on to borrowers will depend on the banks.”

If banks choose to pass on the entire 25 bps reduction to borrowers, the impact on loan EMIs can be significant.

For example:

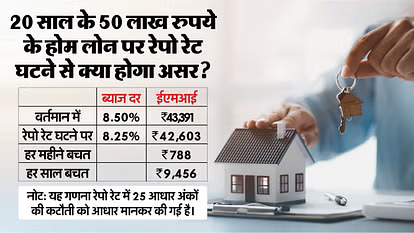

- A borrower with a ₹50 lakh home loan at 8.5% interest for 20 years currently pays an EMI of ₹43,391. After the 0.25% rate cut, if the interest reduces to 8.25%, the new EMI will be ₹42,603, resulting in a monthly saving of ₹788 or an annual saving of ₹9,456.

- A borrower with a ₹5 lakh car loan at 12% interest for five years currently pays an EMI of ₹11,282. If the bank reduces the interest rate by 0.25%, the new EMI will be ₹11,149, saving ₹133 per month or ₹1,596 per year.

Why Did RBI Cut the Repo Rate?

Economic analysts and financial experts had anticipated a rate cut due to several factors:

- Controlled Inflation: According to economic research firm PL Capital Group, retail inflation (CPI) stood at 5.2% in December 2024 and is expected to decline further to 4.5%-4.7% in the coming months. With inflation under control, the RBI found room to ease interest rates.

- Slow Economic Growth: India’s GDP growth for FY 2025 is projected at 6.4%, significantly lower than 8.2% in FY 2024. To stimulate growth, the RBI decided to cut interest rates, making credit cheaper for businesses and consumers.

- Liquidity Concerns: The banking sector has been experiencing a liquidity crunch, prompting the RBI to inject funds into the economy by reducing borrowing costs.

Government’s Role in Economic Growth

The Indian government has been focusing on boosting economic growth through fiscal measures. In the Union Budget 2025-26, the government increased the income tax exemption limit to ₹12 lakh, aiming to enhance disposable income and boost domestic consumption. This move, coupled with lower borrowing costs, is expected to strengthen demand and drive economic recovery.

What’s Next?

While the RBI’s repo rate cut is a welcome move for borrowers, its effectiveness will depend on how banks respond. If financial institutions pass on the benefits to consumers, home and car loan EMIs will reduce significantly, stimulating spending and investment in the economy.

With this policy shift, the central bank has signaled its focus on economic growth while maintaining financial stability. The coming months will determine how this rate cut impacts credit availability and overall economic momentum in India.